As the final quarter of the year approaches, Spain’s residential real estate market continues to advance steadily, although signs of stabilization are beginning to emerge. This is one of the main conclusions of Urbanitae’s Third Quarter 2025 Report, which analyzes the evolution of prices, transactions, rentals, and development activity across the country.

After more than two years of monetary tightening, the European Central Bank’s gradual relaxation of interest rates has begun to ease households’ financial pressure. The average rate for new mortgages reached 2.94% in July, boosting credit activity and supporting housing demand, which remains strong despite a slight slowdown in overall market activity.

However, the imbalance between supply and demand persists. The Bank of Spain estimates a deficit of around 700,000 homes that the market is unable to meet. Limited land availability, high construction costs, and complex administrative processes continue to constrain the sector’s response capacity, especially in major cities.

Prices at Record Levels and a Structural Imbalance

Home prices continue to rise. According to Tinsa, the average value of new and existing homes increased by 11.7% year-on-year in the third quarter, confirming ongoing pressure on available housing stock. Despite a rebound in new construction — with over 84,000 building permits issued through July, up 10.9% compared to 2024 — supply remains far from meeting demand, keeping prices under strain.

This imbalance is compounded by a growing affordability problem. In 2024, average home prices rose 11.3%, while wages increased only 3.8%, according to INE data. The widening gap between income and housing costs makes homeownership increasingly difficult, particularly for young and middle-income households. As a result, housing is becoming more inaccessible and reinforcing its role as a safe-haven asset for investors.

Sales and Rentals: Stabilization and Parallel Pressures

The housing sales market is showing a natural adjustment after several quarters of sustained growth. In August, transactions fell 3.5% year-on-year — the first drop in more than a year — reflecting high prices and limited availability in high-demand areas.

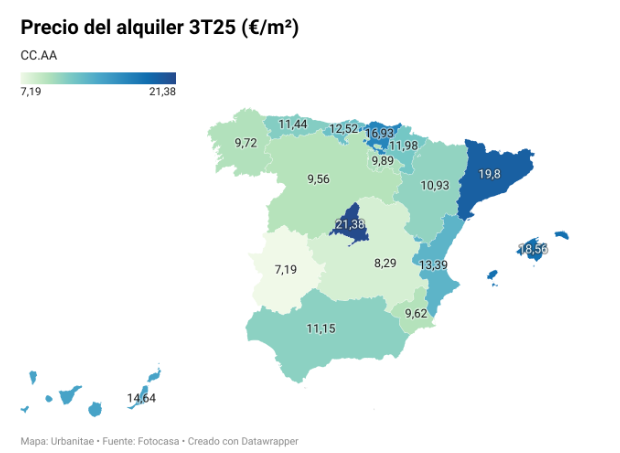

Conversely, the rental market remains at record levels, with an average price of €13.69/m² per month. Although a slight quarterly correction was recorded (-4.8%), annual increases remain around 14%, driven by the lack of available rental housing in large urban centers.

As a result, more families and small investors are moving to nearby municipalities or metropolitan areas, where purchase costs are lower and yields more attractive. This shift is reshaping the residential landscape and redistributing demand across regions.

A Multi-Speed Market

The report identifies three distinct regional dynamics:

- Red light: Madrid (+19.4%), Málaga (+15.3%), and Alicante (+15.3%) lead the price increases, driven by investment and international demand.

- Yellow light: Cáceres, Palencia, and León record moderate growth of around 2%.

- Green light: Zamora (-0.9%) is the only province showing declines, in a context of weak demand and demographic aging.

Outlook: A Moderate but Sustainable End to the Year

Looking ahead to the end of 2025, forecasts suggest a gradual moderation in price growth, accompanied by stable sales activity and continued pressure in the rental market. According to CaixaBank Research, housing prices are expected to rise by 9.6% in 2025 and 6.3% in 2026, signaling a shift toward more sustainable growth.

With GDP projected to grow by 2.6%, inflation at 2.5%, and unemployment around 10.5%, Spain’s economy will continue to provide a stable backdrop for real estate activity — though boosting residential supply remains essential to restoring balance in the market.