The first quarter of 2026 confirms that the Spanish residential market continues to be supported by strong demand, but is increasingly constrained by a structural supply problem. Prices continue to rise, the rental market remains under pressure, and affordability is becoming one of the sector’s biggest challenges.

Despite rising international economic and geopolitical uncertainty, the Spanish residential market continues to show remarkable resilience. Strong employment levels, population growth, Spain’s appeal as a place to live and invest, and the shortage of available product continue to support activity. However, these same factors are also worsening one of the market’s major imbalances: demand continues to grow faster than the sector is able to absorb through new supply.

As Diego Bestard, CEO of Urbanitae, points out in his analysis included in the report, “the first quarter of 2026 has confirmed that this imbalance not only continues, but is intensifying in many markets.” The key issue is that this is not a temporary tension, but a structural problem: fewer homes are being built than the market demands.

A start to the year shaped by uncertainty

The beginning of 2026 has come within a more complex macroeconomic environment than much of 2025. After a year marked by the gradual easing of interest rates in Europe, the first quarter once again introduced caution into financial markets.

The resurgence of geopolitical tensions, energy price volatility and doubts surrounding the evolution of inflation have renewed uncertainty regarding the pace at which the European Central Bank may continue easing monetary policy.

In Spain, year-on-year CPI rose from 2.3% in January and February to 3.3% in March, driven mainly by energy prices. At the same time, the Euribor showed renewed upward pressure during the final stretch of the quarter, reflecting market caution regarding future interest rate cuts.

Even so, the Spanish economy continues to outperform many other European economies, supported by employment, population growth and the strong performance of the services and tourism sectors. All these factors continue to underpin residential demand.

Prices: strong increases spreading more widely

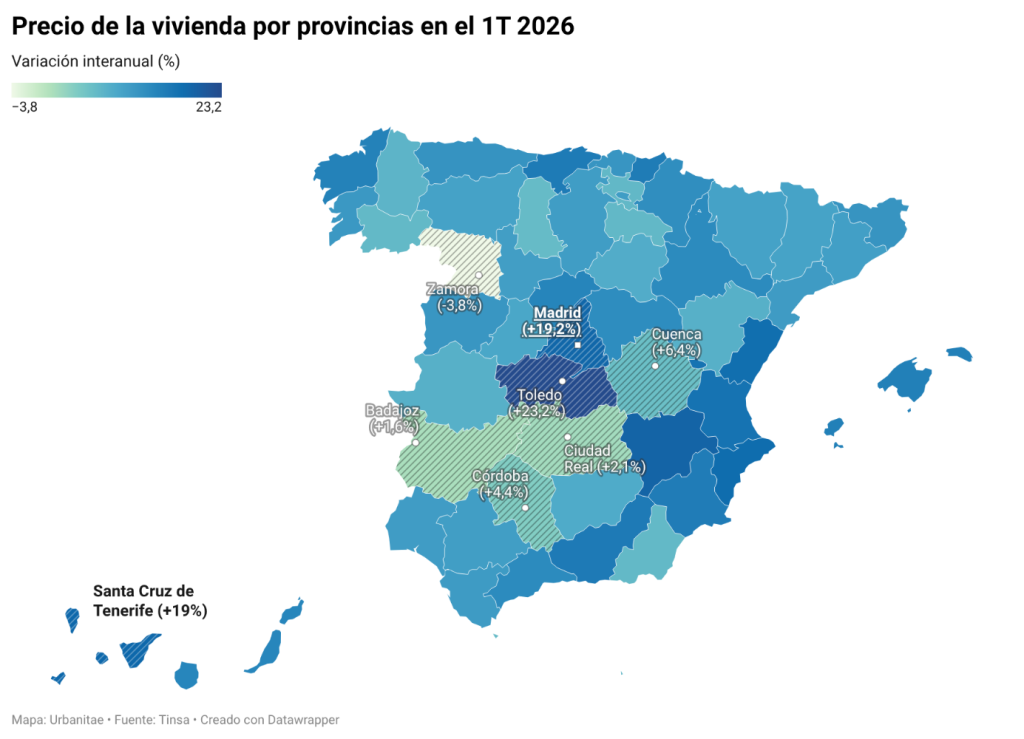

Housing prices started 2026 with further increases. According to Tinsa, the average value of completed housing – both new-build and second-hand – rose by 14.3% year-on-year and 3.2% quarter-on-quarter in the first quarter. In real terms, adjusting for inflation, growth reached 11.8%.

The pressure is no longer limited to traditional hotspot markets. Although Madrid, Barcelona, the Balearic Islands, the Canary Islands and the Mediterranean coast continue to concentrate much of the tension, price increases are spreading to peripheral provinces and secondary markets that are absorbing demand displaced by the high prices in major cities.

Tinsa notes that 14 out of Spain’s 19 autonomous communities and cities recorded year-on-year increases above 10%. The largest increases were seen in the Community of Madrid (+19.2%), Valencian Community (+19.1%), Castilla-La Mancha (+18.8%), Canary Islands (+17.8%) and Cantabria (+16.2%).

At provincial level, standout increases include Toledo (+23.2%), Albacete (+19.6%), Madrid (+19.2%), Santa Cruz de Tenerife (+19.0%) and Alicante (+18.3%). The case of Toledo is particularly significant, reflecting the shift of part of the demand from Madrid towards more affordable, better-connected areas with some remaining absorption capacity.

In the major cities, pressure remains intense. Madrid recorded a year-on-year increase of 17.9%, while Barcelona reached 11.5%. Together with San Sebastián, both cities now exceed €4,000 per square metre, consolidating their position as the country’s most expensive residential markets.

Transactions moderate, but remain at high levels

Residential activity remains strong, although it is beginning to show signs of moderation compared to the intense momentum of recent years. According to Spain’s Land Registrars Association, 178,096 home transactions were recorded in the first quarter, representing a slight quarter-on-quarter decrease of 0.1%. On a year-on-year basis, cumulative transactions reached 701,828 deals, down 1.9%, but still at their highest level since the third quarter of 2007.

By segment, performance was uneven. New-build housing transactions rose by 7.2% quarter-on-quarter, reaching 39,473 transactions, while second-hand housing declined by 2%, with 138,623 transactions. The shortage of new-build product continues to concentrate demand wherever supply exists, particularly in areas with strong economic and tourism activity.

Foreign demand also remains highly relevant. In the first quarter, foreign buyers accounted for 13.92% of total home purchases, representing nearly 24,800 transactions. The highest shares were recorded in the Balearic Islands (28.89%), Valencian Community (28.16%), Canary Islands (22.78%) and Region of Murcia (21.73%).

The rental market remains under pressure

The rental market continues to be one of the most strained segments. Difficulty accessing home ownership, especially for younger households and those with lower savings capacity, continues to push demand towards renting. At the same time, available supply remains limited across many markets.

According to Fotocasa, average rental prices rose by 4% quarter-on-quarter and 9.1% year-on-year in the first quarter, reaching €14.78 per square metre per month. Idealista, meanwhile, estimates annual growth at 7.1%, with average rents close to €15 per square metre.

The strongest pressures remain concentrated in Madrid, Catalonia and the Balearic Islands, although tension is increasingly spreading to other regions. Fotocasa highlights quarterly increases in Cantabria (+11.1%), Aragon (+6.9%), Community of Madrid (+6.7%), Valencian Community (+5.9%) and Andalusia (+5.6%). Idealista identifies Castilla-La Mancha as the region with the highest annual increase, at 12.7%.

The most relevant factor is not only that prices continue to rise, but that the market’s absorption capacity is beginning to narrow. In many areas, rents are increasingly disconnected from household purchasing power, which could moderate the pace of growth, although not necessarily ease overall market tension.

This is not a bubble, but a supply problem

One of the report’s key conclusions is that the current cycle differs significantly from the period preceding the 2008 financial crisis. Although prices are rising sharply and activity remains elevated, the market is not facing excessive construction or widespread overleveraging.

The problem is different: supply is not growing at the same pace as demand. The shortage of development-ready land, rising construction costs, administrative complexity, labour shortages and lengthy development timelines are limiting the sector’s ability to deliver new housing.

Diego Bestard summarises this in his quarterly outlook: “I do not see a scenario of abrupt correction, but I do believe the market is entering a phase in which affordability will become increasingly decisive and in which not all demand will be able to materialise.”

This diagnosis also explains the growing interest in residential models complementary to traditional build-to-sell, such as flex living, senior living and coliving. These models do not replace conventional housing, but they do respond to real shifts in demand: smaller households, greater mobility, new working needs and the search for flexibility and services.

Financing: an increasingly relevant piece of the puzzle

The report also highlights the central role of financing in this new cycle. Banks remain the cornerstone of the system, but the market increasingly requires more flexible structures, especially during the early phases of projects.

According to the updated Real Estate Development Financing Observatory produced by Urbanitae together with KPMG, total investment volume in real estate development increased from around €35 billion in 2024 to nearly €39 billion in 2025. At the same time, alternative financing has continued to gain scale and sophistication.

For Urbanitae, this evolution confirms that non-bank capital has become a structural tool to complement traditional banking, provide agility and allow viable projects to move forward rather than becoming blocked by financing gaps during certain phases.

Outlook: continuity, but with greater caution

Looking ahead to the second quarter, the outlook points more towards gradual moderation than a sharp shift in trend. Demand will continue to be supported by solid fundamentals – employment, population growth, international appeal and limited supply – but inflation, interest rates and geopolitical uncertainty could introduce greater caution, especially among buyers dependent on mortgage financing.

The shortage of available product will remain the market’s main source of tension. Although development activity is showing signs of improvement, with a 19.6% increase in newly approved projects according to Tinsa, production levels remain insufficient to meet existing demand.

The first quarter of 2026 therefore leaves a clear picture: the Spanish residential market remains active, but increasingly demanding. Demand remains resilient, prices continue to rise and affordability continues to deteriorate. Resolving this imbalance will require unlocking land, streamlining administrative processes, expanding financing sources and developing new residential models capable of responding to increasingly diverse demand.

Read the full report here: