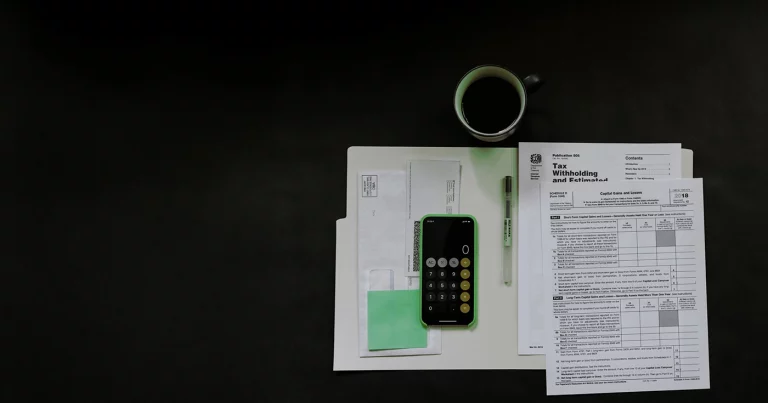

2025 Income Tax Campaign: Updates on Housing

Deductions for rental properties and energy efficiency renovations are among the main new features of the 2025 tax return campaign related to housing.

income tax

Deductions for rental properties and energy efficiency renovations are among the main new features of the 2025 tax return campaign related to housing.

Changes in taxation, adjustments to incentives, and new measures like the reduction of ITP for young people make it crucial to understand how these modifications impact your investment decisions.

How Urbanitae investments are taxed: interest, equity, withholdings and key points to understand what to declare and how to do it correctly.